Consumer-driven Underinsurance

How can employers and payers better support patients as high-deductible health plans rise and coverage falls?

A few years ago, a woman fell and was trapped between the subway platform and the train. Her fellow passengers were able to free her but the story made national headlines because she didn’t want anyone to call an ambulance as she couldn’t afford it. She made it a point to say “You don’t understand, I have terrible insurance”. And though she ultimately agreed to go with the EMTs to the hospital to receive surgery this story is a sobering reminder of the 44 million uninsured and underinsured Americans that have been struggling even more since the downturn of COVID-19.

What does being underinsured actually mean? In layman’s terms, an individual or family who is underinsured has insurance that doesn’t ultimately doesn’t adequately cover their health needs. The Commonwealth Fund defines underinsurance for people where out-of-pocket health care costs took up between 5% and 10% of their annual incomes, or if their health plans' deductibles equal more than 5% of their annual incomes.

You might wonder if the Affordable Care Act wasn’t created to tackle exactly this, right? And you would be right - the ACA made great strides in reducing the uninsured population. However just because more people now have insurance doesn’t mean that it’s adequately serving the needs of the underinsured.

High-deductible Health Plans and Underinsurance

About 42 percent of people with individual health coverage said they were underinsured in 2018, compared with 28 percent of those with job-based coverage. Yet from 2010 to 2018, the greatest growth in the underinsured rate was among adults with employer-based plans.

While plans in the employer market historically have provided greater cost protection than plans in the individual market, businesses have tried to hold down premium growth by asking workers to shoulder an increasing share of health costs, particularly in the form of higher deductibles. While the ACA’s employer mandate imposed a minimum coverage requirement on large companies, the requirement amounts to just 60 percent of a typical person’s overall costs. This leaves the door wide open for high-deductible plans and copayments.

In order to meet the ACA’s employer mandate, many employers began pushing employees to adopt high deductible health plans which were more affordable due to lower premiums but featured higher deductibles. High-deductible health plans (HDHPs) mean that employees pay more out of pocket healthcare costs before meeting the deductible where an insurer will start footing the bill - a particularly alarming ask especially in the wake of unpredictable healthcare emergencies.

When HDHPs first came out, many anticipated that it would drive more “consumerization of healthcare”. And while the patient is indeed behind the steering wheel of healthcare decisions, it turns out uninsurance leads many to put the brakes on their healthcare needs entirely. This study found that both high-income and low-income women in HDHPs delay breast cancer treatment.

Underadoption of HSAs

The other frequently cited suggestion for working Americans are health savings accounts - pre-tax contributions employees can make towards an account specifically earmarked for healthcare expenditures, where contributions can be invested and grow tax-free.

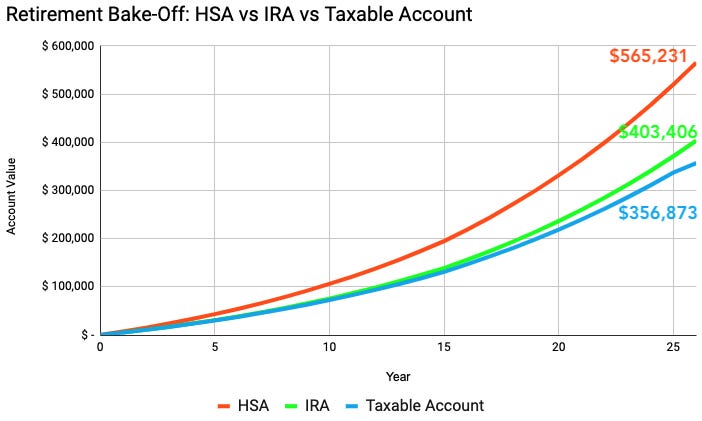

In theory, this is an amazing (and very utilized) savings mechanism. The graph below shows how the same regular investment compares against an IRA and taxable brokerage account. As employees age, HSA savings and tax-free gains can be helpful just when they need them later in life.

This study found that 1 in 3 Americans on a HDHP do not have a HSA. And even among those that do, more than half did not contribute any money to the HSA in the last 12 months. Perhaps unsurprisingly, many patients cited “ did not need healthcare” or “already had savings” as being the main reason for not contributing to an HSA.

HDHP-HSAs and Chronic Conditions

Part of what gets me fired up about this issue is that HDHPs don’t provide the proper incentives for patients with chronic diseases or who otherwise need more healthcare services to effectively manage their health. Only last year did policymakers pass the Chronic Disease Act which allowed HDHP-HSA plans to cover preventative medicines to manage diabetes, asthma, hypertension, depression - essential medications that patients would otherwise ignore because they came out of out-of-pocket costs. Even so, HDHPs and HSAs alone don’t prepare patients for unforeseen or chronic healthcare needs. The bottom line is that HDHPs lead patients to drive down healthcare utilization including necessary preventative measures - changing their health care behavior to save money and forgo needed care.

There’s more promising tailwinds that the Biden administration seems to be advocating for - making higher-tier plans on the ACA marketplace more affordable by expanding subsidies and extending eligibility for patients that already have employer coverage. However, we also need to explore ways to improve coverage outside of the employer marketplace. There are many systemic problems related to lack of Medicaid expansion and patients that fall into a coverage gap due to lost jobs since the pandemic - but this is a topic for another post!

In the meantime, are there ways we might incentivize and motivate patients to use HDHP-HSAs to properly prepare for their chronic conditions?

Idea: Tying Predicted Healthcare Expenditures to Employer-sponsored HSAs

I wonder if there are lessons we can take from employer-driven financial savings to lower the consumer energy barrier to encourage healthcare savings. In other words, what would a personalized 2060 target retirement plan look like in the healthcare context?

Self-insured employers could use healthcare claims data to predict and personalize suggestions for their employees based on their past healthcare usage. And employers could incentivize the right proactive behaviors through employer-sponsored matching of funds to HSAs. There would be cost-savings for both employers and employees from driving earlier and more comprehensive healthcare savings based on the personalized healthcare needs of each employee.

Some insurers are already leaning into a similar model by designing plan structures that incentivize usage of preventative services. Aetna’s Upfront Advantage plan gives access to preventative services worth up to $500 for an individual and $1,000 for a family for free before their deductible is met. In another structure they call the Flexible Five, members will instead be offered five coupons per person for preventative services; a family of four, for example, would receive 20 coupons that can be applied to services such as primary care visits, behavioral health visits, urgent care, lab tests or x-rays conducted during those visits and generic drugs.

Both these employee-facing and payer-sponsored approaches could be used in tandem to better drive employees and employers to incentivize investment into more preventative and longitudinal services.

Would love to hear thoughts from others - especially those that have been on HDHP-HSAs themselves. What are other ideas to better align employee/patient needs in the context of employer-sponsored insurance?

Thanks to Akaash for helpful suggestions in early drafts of this piece, and to Dr. Kevin Thorpe and the authors behind this Health Affairs piece which inspired a lot of this thinking.